Can the DoD Actually Spend $1–1.5 Trillion Effectively? Yes—But Only If It Changes Who Gets the Money

The debate around the Department of Defense’s future budget has quickly escalated from incremental increases to something far more ambitious. Senior administration officials and policy voices have openly discussed pushing the defense budget toward—or beyond—$1 trillion annually, with some projections for FY27 reaching as high as $1.5 trillion[i]. That shift raises a more important question than the topline itself:

Can the Department of Defense actually absorb that level of capital effectively?

The conventional answer in some Washington circles has been “no,” citing industrial base constraints, acquisition delays, and execution risk. But that answer is incomplete. The real answer is:

Yes—but only if the DoD fundamentally changes how and where that capital is deployed.

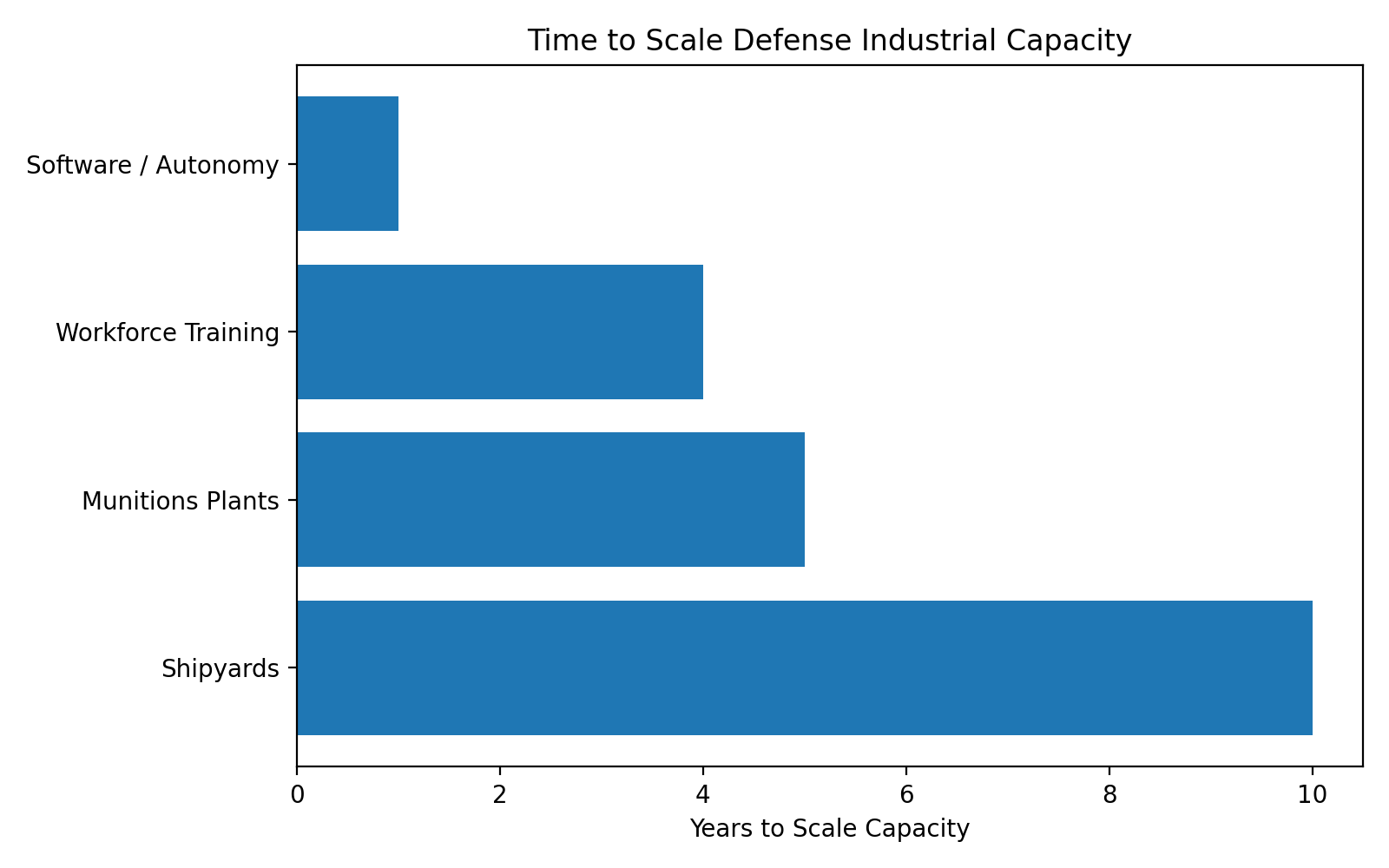

The Absorption Problem Is Real—but Misdiagnosed

There is no question the defense ecosystem faces real constraints:

Shipbuilding capacity is maxed out[ii]

Munitions production scales in years, not quarters[iii]

Prime contractors operate on long-cycle program timelines[iv]

Workforce and supply chains remain bottlenecks[v]

These constraints have led many analysts to conclude that a $1T+ defense budget would result in diminishing returns; more dollars chasing the same constrained capacity.

At the same time, the United States has already begun shifting toward re-industrialization, reshoring, and supply chain resilience—particularly across defense-critical sectors. This shift is directionally correct.

Over the past several years, policymakers and industry have:

Prioritized domestic production capacity for munitions and critical components

Invested in onshoring key elements of the defense supply chain

Emphasized resilience over efficiency in industrial planning

However, this transition is still in its early stages.

Rebuilding industrial capacity is not a near-term solution, it is a multi-year, and in many cases multi-decade effort. Shipyards cannot be expanded overnight. Skilled labor pipelines take years to develop. Supplier ecosystems require sustained demand signals to mature. The result is a temporary but important dynamic: policy is moving faster than industrial capacity can respond.

This gap reinforces the perception that additional defense spending will struggle to translate into near-term capability. But it also creates something else: a generational investment opportunity in rebuilding the defense industrial base.

This is a core focus area for Veteran Ventures Capital. We actively seek and support companies that sit at the intersection of advanced manufacturing, dual-use technologies, and national security, particularly those that can accelerate the reshoring and modernization of critical supply chains.

As capital continues to flow into industrial resilience, the companies best positioned to benefit will be those that:

Can scale production faster than legacy suppliers

Leverage modern manufacturing techniques and automation

Integrate software, autonomy, and advanced materials into traditional industrial processes

These are not just policy priorities, they are investable trends.

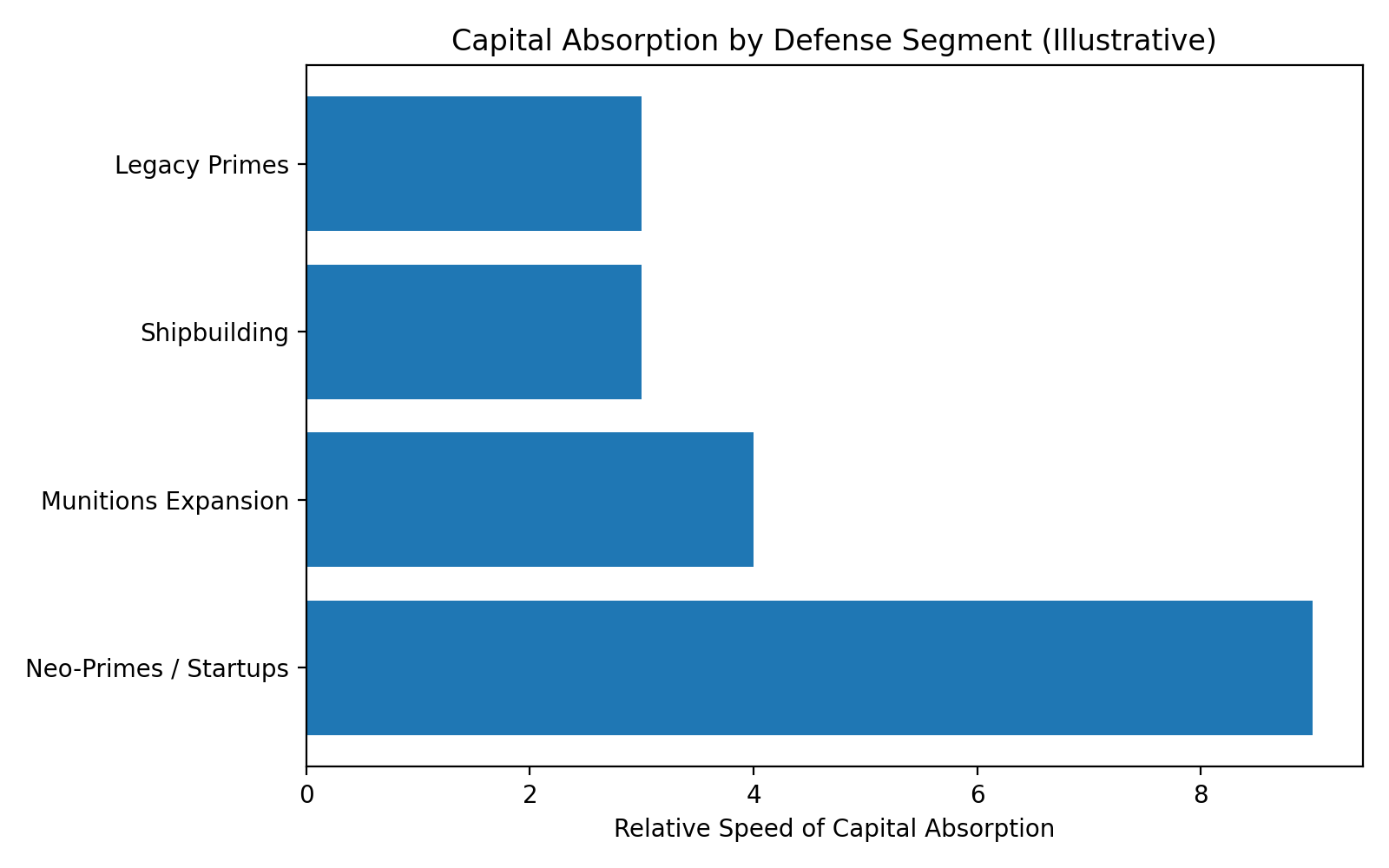

The Real Bottleneck: Legacy Allocation, Not Total Capacity

The U.S. defense industrial base is not monolithic. It consists of two very different systems:

1. Defense Primes (Traditional System)

Slow capital deployment

Long-cycle programs

Limited short-term scalability

2. Emerging Defense Tech / Neo-Primes (New System)

Faster capital absorption

Shorter development cycles

Scalable architectures

The absorption problem is not that DoD cannot spend more money. It is that the traditional system cannot absorb incremental capital efficiently (although these defense primes are undergoing a transformation of their own to catch up to the new system, but this too takes time).

Acquisition Reform and Money Flow Is the Unlock

Over the past several years, the Department has begun shifting how it acquires capability:

OTA expansion

SBIR/STTR transition scaling

Commercial solutions pathways

Software acquisition reforms

Veteran Ventures Capital has operated at the center of this shift. Across our portfolio, companies have secured hundreds of millions in non-dilutive funding through these pathways. We don’t just invest, we help companies navigate acquisition regulations, align to mission demand, and capture non-traditional funding. This is what allows capital to move faster.

More capital (both governmental and private) must go toward:

Advanced Materials

Software-defined systems

Autonomy and robotics

Space + ISR

AI

These are the exact areas where VVC invests today—because they absorb capital faster, scale faster, and deliver capability faster. The venture-backed ecosystem is now a necessary component of the DoD’s ability to scale spending effectively; absent it, systemic bottlenecks will persist.

Summary and Our Conclusion

The question facing the Department of Defense is no longer whether it can secure a $1T—or even $1.5T—budget. It is whether the system responsible for deploying that capital is built for scale. As the Department works to adapt, capital will increasingly flow toward companies that can absorb and deploy it efficiently. Veteran Ventures Capital’s portfolio is built for exactly that environment.

References

[i]https://breakingdefense.com/2026/03/with-the-pentagons-fy27-budget-request-forthcoming-its-unclear-if-it-will-hit-1-5-trillion/

https://federalnewsnetwork.com/congress/2026/03/a-1-5t-dod-budget-in-a-split-congress-would-demand-prime-political-maneuvers/

[ii] CSIS, shipbuilding capacity constraints and naval industrial base

https://www.csis.org/analysis/what-can-trumps-budget-buy-navy-exploring-options-and-trade-offs

[iii] CSIS / DoD reporting on munitions ramp timelines

https://www.csis.org/analysis/rebuilding-us-inventories-six-critical-systems

[iv] GAO, defense acquisition cycle timelines

https://www.gao.gov/products/gao-25-106036

[v] DoD Industrial Base Report / workforce + supply chain constraints

https://media.defense.gov/2024/Nov/14/2003582337/-1/-1/1/2024-DOD-INDUSTRIAL-BASE-REPORT.PDF