Defense Tech’s $86 Billion Waiting Room Has a Third Exit

Three years ago, defense tech had two ways out: get acquired or wait. A third path now exists. Most of the sector doesn’t know how to build for it yet.

For most of the history of defense tech venture, exit was a binary problem. You sold the company to a prime contractor or a PE platform, or you waited. The IPO window opened occasionally for the rare company that could clear the bar. Secondary liquidity was theoretical — something that happened to other sectors. That changed. Over the past three years, SpaceX normalized the tender offer, Goldman Sachs acquired Industry Ventures, Morgan Stanley acquired EquityZen, and Schwab acquired Forge Global.¹⁸ Wall Street built the infrastructure for large-scale private equity liquidity before most of defense tech recognized what was being constructed. In 2025, for the first time, secondary volume in venture broadly crossed above IPO exit value. Three exit channels are now active simultaneously. Defense tech is not yet at parity across them — secondary liquidity today pools heavily in the top five names — but the architecture exists, and the conditions required to access it are buildable from the first check. That is what this article is about.

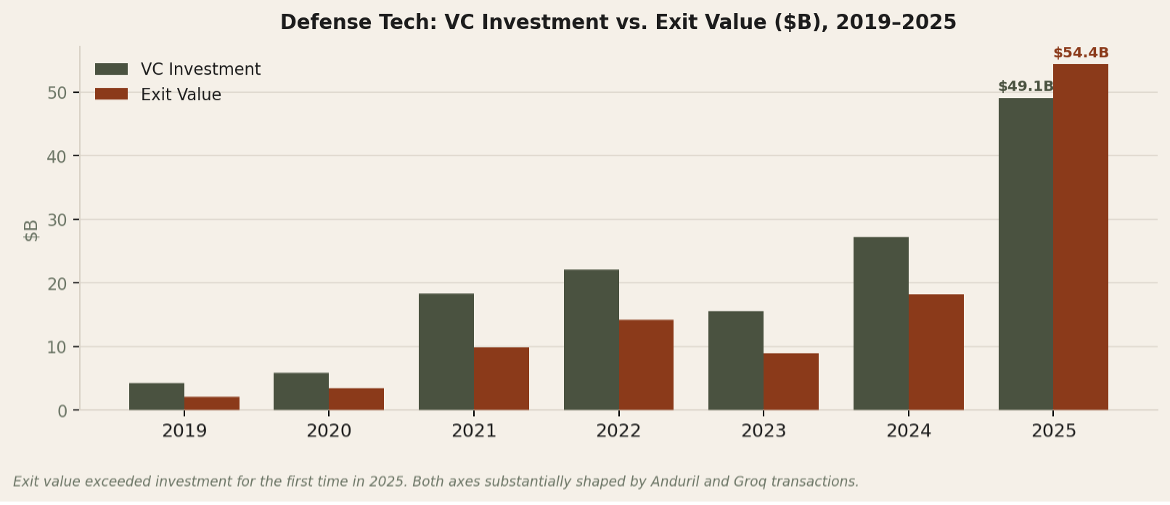

First, the headline numbers, because they require reading before they are useful. Venture capital investment in defense technology reached $49.1 billion in 2025, nearly doubling from $27.2 billion in 2024.¹³ Exit value surged to $54.4 billion from $18.2 billion.¹⁹ Both figures are real. Both are substantially shaped by transactions at the very top of the distribution: Anduril’s $2.5 billion Series G, which represented roughly 5% of total annual defense tech investment by itself,¹³a and Nvidia’s approximately $20 billion non-exclusive IP licensing transaction with Groq, whose primary 2025 revenue driver was a $1.5 billion Saudi Arabia commercial AI infrastructure commitment, not a US defense contract.³⁸,³⁸a Strip both and what remains is still a record year for the 95% of the sector not named Anduril or Groq — but a materially different picture. The NatSec100’s top 100 venture-backed defense companies have raised $70.1 billion in private capital against $28 billion in cumulative federal awards.⁴⁰ That investment-to-revenue gap is the real constraint on exit timelines, and it is exactly what the third exit path changes for companies that build correctly for it.

Fig. 1 Defense Tech: VC Investment vs. Exit Value ($B), 2019–2025 — For the first time in 2025, exit value exceeded capital deployed. The concentration caveat applies to both axes. [Chart available in HTML/PDF version]

The Third Exit

How Secondary Liquidity Came to Defense Tech, and What It Requires

SpaceX did not set out to build infrastructure for the defense tech secondary market. It did so as a byproduct of its own capital needs. Three completed tender offers — at $350 billion, $400 billion, and $800 billion — forced Goldman, Morgan Stanley, and institutional buyers to develop the documentation templates, diligence frameworks, and valuation methodologies for large-scale private national security equity.² That work does not disappear between SpaceX tenders. It is available to the next defense tech company that can meet the conditions institutional secondary buyers require. The question — for every GP and every LP evaluating a GP — is whether the portfolio is being constructed to meet those conditions.

The conditions are specific and they are not accidental. Secondary buyers underwrite three things in a private defense tech company: demonstrated recurring government revenue with visible renewal probability, a cap table with credible institutional and strategic co-investors who validate the company’s acquisition attractiveness, and a preference stack that does not make the math impossible. All three are construction decisions made at the earliest stages of a company’s life, years before any secondary buyer appears. A GP that does not think about secondary conditions at the Series A is not thinking about the full exit architecture.

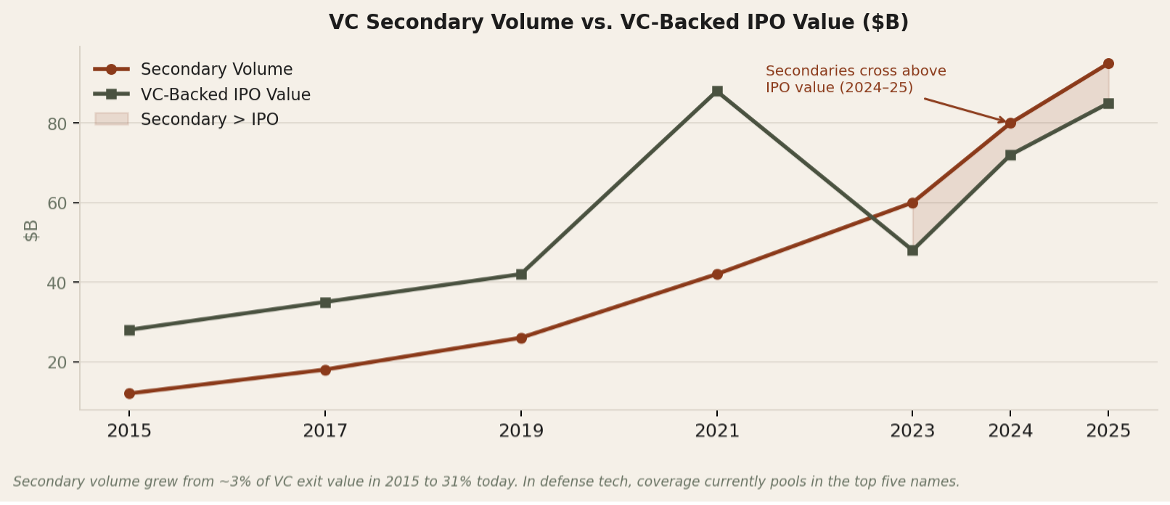

Anduril already trades robustly in secondary markets at implied valuations above its formal round price.⁴¹ The five or six names with that access today represent a proof of concept, not a ceiling. Tomasz Tunguz documented in February 2026 that secondary volume across venture broadly has grown from roughly 3% of exit value in 2015 to 31% today, absorbing nearly $95 billion in the trailing twelve months.¹⁸ The institutional infrastructure that drove that shift is now permanent. The coverage gap in defense tech — the distance between Anduril and the rest of the sector — will close as more companies reach the revenue and cap table conditions secondary buyers require. GP-led continuation vehicles are the near-term bridge for companies approaching but not yet at that threshold. The question is which portfolios are structured to reach it.

-

Demonstrated recurring government revenue with visible renewal probability. A cap table with credible strategic co-investors who validate acquisition attractiveness. A preference stack that does not make the math impossible. All three are early-stage construction decisions. A GP not thinking about them at Series A is not building for the full exit architecture.ription text goes here

Fig. 2 VC Secondary Volume vs. VC-Backed IPO Value ($B) — Secondaries crossed above IPO value in 2024 and 2025 — a structural shift, not a cyclical one. In defense tech, coverage today pools in the top five names. Expanding that is the structural opportunity for the next cohort. [Chart available in HTML/PDF version]

Acquisitions

The Known Channel, Now Running Wider

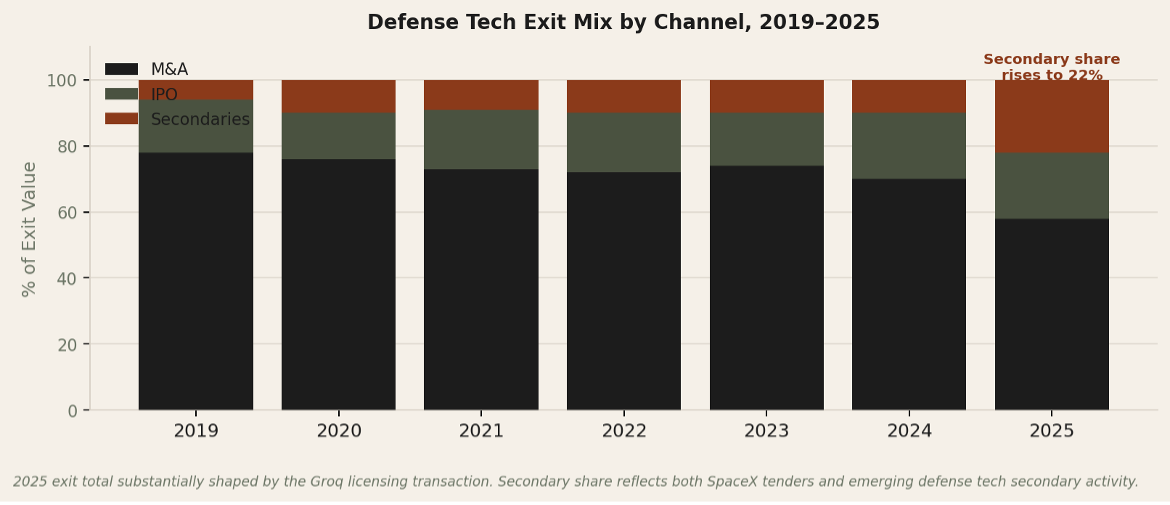

M&A has historically accounted for roughly 72% of defense tech exits by value¹ and it remained the dominant channel in 2025, with 125 transactions in Q3 alone, up 30% year over year.⁴² The acquirer universe has expanded materially. Legacy primes co-investing at Series A — establishing acquisition optionality before a program of record exists — is now standard practice. When VVC co-invested alongside Lockheed Martin Ventures, SAIC Ventures, and Airbus Ventures in Vatn Systems’ December 2025 Series A,¹⁵ those primes became option holders with a multi-year head start on any competitor bidding at growth stage. Applied Intuition’s acquisition of EpiSci added neoprime-to-neoprime consolidation to the pattern: a $6 billion autonomy platform acquiring adjacent AI capability rather than building it.⁴³ Redwire’s $925 million acquisition of Edge Autonomy completed the PE-to-strategic-acquirer cycle.⁴⁴ And European defense M&A grew from $2.6 billion to $8.1 billion in 2025,⁴⁵ adding a buyer cohort that did not meaningfully exist two years ago. The total acquirer universe — legacy primes, scaling neoprimes, public defense tech companies, PE platforms building for strategic sale, and European strategics — has not been wider. The strategic co-investor at Series A is the M&A pipeline. That is also the secondary market condition. The two exit paths share the same construction logic.

Private equity operates as a structural mid-market layer within M&A. Specialist firms like Veritas Capital, which closed Fund IX at $14.4 billion in September 2025, and Arlington Capital, which closed Fund VII at $6 billion in October and sold its BlueHalo/Eqlipse platform to AeroVironment for $4.1 billion,⁵⁷,⁵⁸ have been executing the build-and-sell playbook through full defense cycles for decades. The constraint is real: defense M&A averages roughly 10 to 12 times EBITDA for mission-critical businesses,⁶⁰ and a venture-scale preference stack can make a PE bid non-executable. The PE layer is active for companies that have reached profitability and manufacturing scale. Getting there is the work.

Fig. 3 Defense Tech Exit Mix by Channel, 2019–2025 — M&A has historically dominated. The sub-categories within it expanded in 2025 as the acquirer universe widened across legacy primes, neoprimes, PE platforms, public acquirers, and European strategics. [Chart available in HTML/PDF version]

Public Markets

Proof of Concept, with an Honest Scorecard

Palantir settled the question of whether dual-use defense tech can reach public market scale. $4.48 billion in 2025 revenue growing 56% year over year, trading at a $330 billion market cap.³⁹ The valuation multiples are extreme and the timeline — twenty-two years from founding — is not a fund model. What Palantir establishes is the architecture: government as anchor customer, commercial as growth multiplier, AI as the margin engine. A SpaceX IPO at a potential $1.5 trillion valuation would add something Palantir alone cannot — permanent institutional analyst coverage and valuation frameworks that benefit every defense tech company that lists after it.¹⁷

The 2025 IPO cohort provided an honest scorecard. Karman Holdings priced at $22 in February and trades near $60 today: profitable hypersonics and missile defense hardware, direct Golden Dome exposure, manufacturing execution. The market rewarded exactly what the thesis predicted.⁵⁴ Voyager Technologies opened at $56 on Starlab narrative, then reverted to its $31 offering price as an 18% revenue growth rate met a 16x price-to-sales multiple.⁵⁵ Firefly fell more than 55% after two hardware mishaps, then used its $868 million raise to acquire SciTec for $855 million — adding missile warning software and Golden Dome positioning while returning Alpha to the pad.⁵,⁵² The public market is not a finish line. It is a capital source with a continuous performance requirement. The companies that understand that before they list will use it differently than those that do not.

Fig. 4 2025 Defense Tech IPO Cohort: Performance vs. Offering Price — Karman has nearly tripled. Voyager reverted to offering. Firefly sits 55%+ below its offering with the $855M SciTec acquisition layered on. (100% = offering price.) [Chart available in HTML/PDF version]

Below the Headline

The Architecture Working at Representative Scale

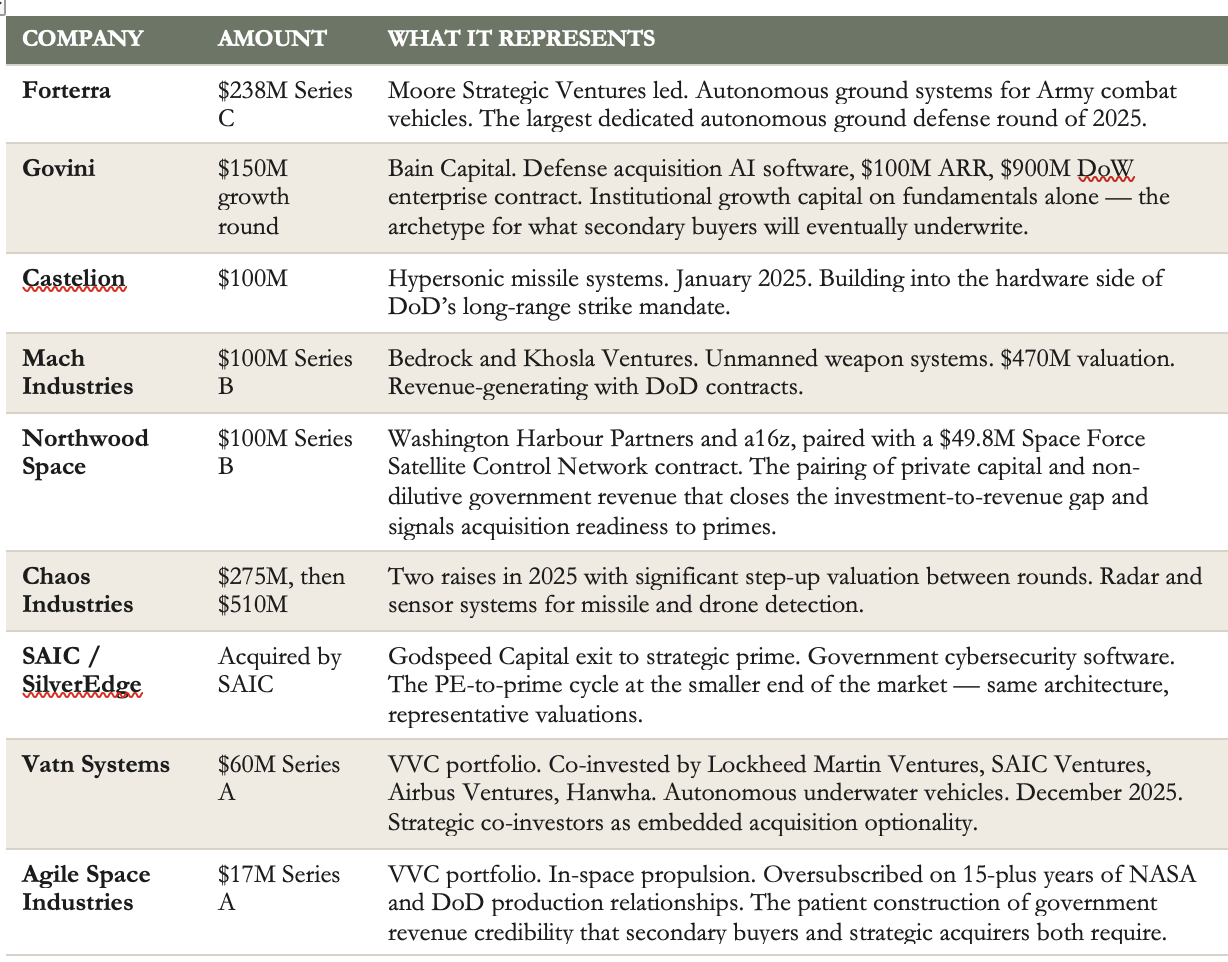

The three channels documented above are not confined to the top of the distribution. The more useful signal for LP purposes is whether the same exit logic operates at valuations representative of most early-stage portfolios. It does. Govini reached $100 million in ARR, secured a $900 million DoW enterprise contract, and closed a $150 million Bain Capital growth round on fundamentals alone.⁶¹ Northwood Space paired a $100 million Series B with a $49.8 million Space Force contract:⁶² non-dilutive government revenue signaling acquisition readiness to primes and secondary buyers simultaneously. SAIC’s acquisition of SilverEdge from Godspeed Capital is the PE-to-prime cycle at the smaller end of the market, no purchase price disclosed, but the pattern clear. The table below is selective. Its purpose is to show that the conditions required to access all three exit channels — government revenue, strategic co-investors, manufacturing credibility — are being met below the headline tier, and to identify what that construction actually looks like.

Looking Forward

What Changed This Week and What Was Already True

On February 28, the United States and Israel launched Operation Epic Fury, conducting strikes against Iranian nuclear and military infrastructure. Iran has retaliated. Defense stocks hit all-time highs on March 2. Palantir’s AIP platform was reportedly used operationally for targeting and intelligence integration — the clearest possible live validation of the dual-use AI model.⁵¹ DoD analysts say the department must triple or quadruple interceptor production rates to replenish THAAD and PAC-3 stockpiles.⁵⁰ Anduril announced its $4 billion raise the same week.

One experienced defense analyst flags that the gains could prove short-lived if the conflict neutralizes Iran as a sustained threat, citing the historical boom-and-bust pattern in defense procurement. That caution belongs in every honest LP update. The durable thesis does not rest on a conflict trade. It rests on the structural shift in how the DoD acquires capability — through non-traditional vendors, at software margins, on faster timelines — that was underway before Epic Fury and will continue after it. DoD spend on NatSec100 companies grew 2.3 times year over year in FY2024.¹⁴ The transition from prototype to program of record is happening, selectively. The companies positioned inside that selection are the ones worth backing.

2026: Four Vectors

Our Position

Building for All Three Exits from the First Check

VVC backs veteran-led, dual-use national security companies from seed through Series A — the stage where the technology is demonstrably real but the revenue story is still early. Our portfolio spans counter-UAS sensing, in-space propulsion, autonomous underwater systems, and advanced materials. We enter before the exit infrastructure is obvious because the return is built at that stage, not captured later. The three-channel framework above is not how we describe our strategy after the fact. It is the architecture we are constructing from the first check.

Before we write a check, we ask three questions. Which acquisition archetype does this company most likely enter, and is the cap table being structured to invite rather than complicate that outcome. What does the path to demonstrated recurring government revenue look like, and how quickly can we unlock non-dilutive capital — SBIRs, STTRs, OTAs — to close the investment-to-revenue gap. And are we building the co-investor base that a secondary buyer would require to underwrite this company two to four years from now. The Vatn Systems syndicate — Lockheed Martin Ventures, SAIC Ventures, Airbus Ventures, Hanwha, BVVC, alongside VVC — was constructed to answer all three questions at once.¹⁵

Agile Space Industries is what patient construction produces. Fifteen years of NASA and DoD relationships, qualified production capacity, and non-dilutive contract revenue positioned the company to close an oversubscribed $17 million Series A in early 2026.¹⁶ That round was competitive not because the technology was newly demonstrated, but because the government revenue record was unimpeachable. The interceptor depletion from Epic Fury and the DoD’s push to triple production rates moves companies with established production relationships from the contracting queue into long-term programs of record. Agile does not need to be in the top five names to access all three exit channels. It needs to meet the conditions. We are building to meet them.

For you as an LP: this sector carries real duration, and we will not minimize that. But the argument of this article is that duration is manageable when the exit architecture is deliberately constructed rather than passively awaited. Three exit channels are active simultaneously in defense tech for the first time. The secondary market — the newest and least understood of the three — is infrastructure without coverage for most of the sector right now. The GPs who understand the conditions required to access it, and build for them from day one, are the ones whose portfolio companies will be first in line when coverage expands. That is our position.